Rockport Market Update – April 2026

Key Takeaways

-

Markets react to Iran conflict and oil prices spike

-

Inflation back on the rise in coming months

-

Rate cuts appear less likely now

-

Stagflation is most likely outcome for the next few days

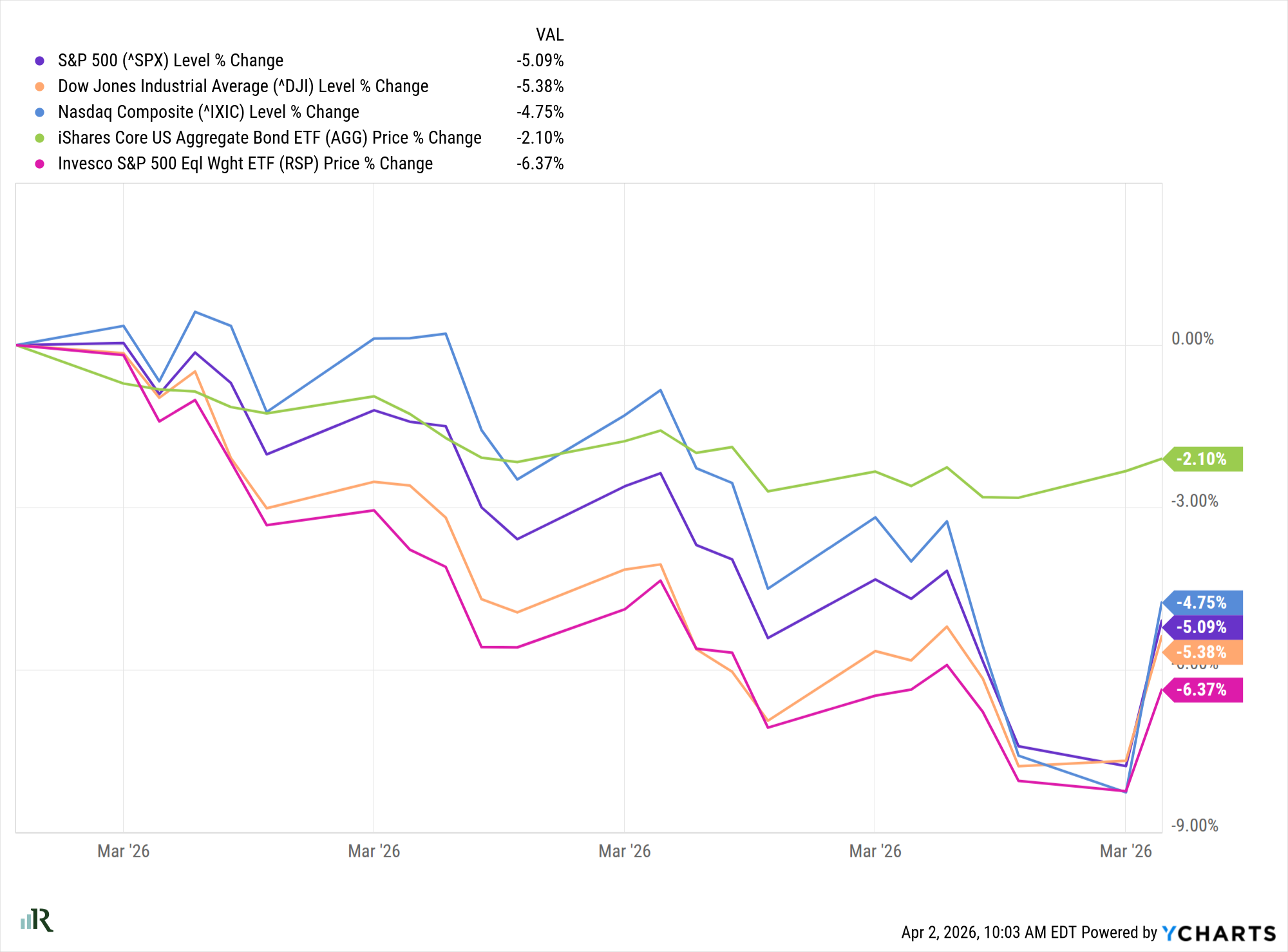

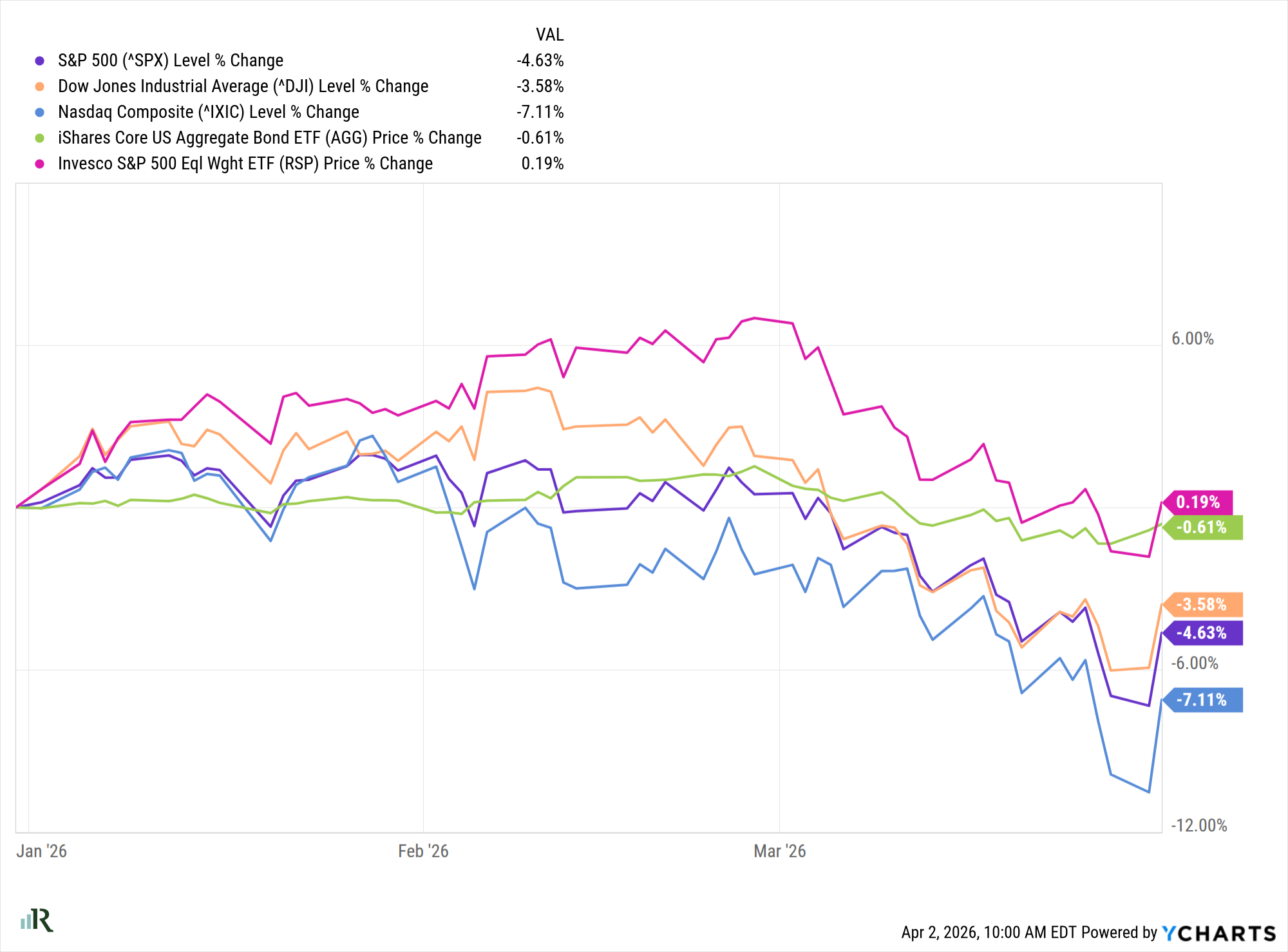

Stock Market Recap

Markets responded to the escalation of conflict involving Iran in March with a meaningful pullback. For the month, the S&P 500 declined 5.09%, bringing its year-to-date return to -4.63%. As is often the case during geopolitical tensions, most major indexes, including international markets, followed a similar downward trend. Notably, even bonds, which are typically viewed as a safe haven during periods of uncertainty, posted negative returns.

Amid the broader weakness, energy stocks and commodities stood out as areas of strength, outperforming the broader market. While the current environment differs in many respects, the recent market pattern is reminiscent of last year’s decline from mid-February through early April, which was driven largely by tariff-related concerns. However, the underlying drivers appear distinct. The current downturn has been influenced more by an oil price shock, whereas last year’s volatility was tied more to market sentiment and uncertainty around potential policy outcomes. Historically, sharp and sustained increases in energy prices have often led to meaningful economic shifts, making this an important development to monitor.

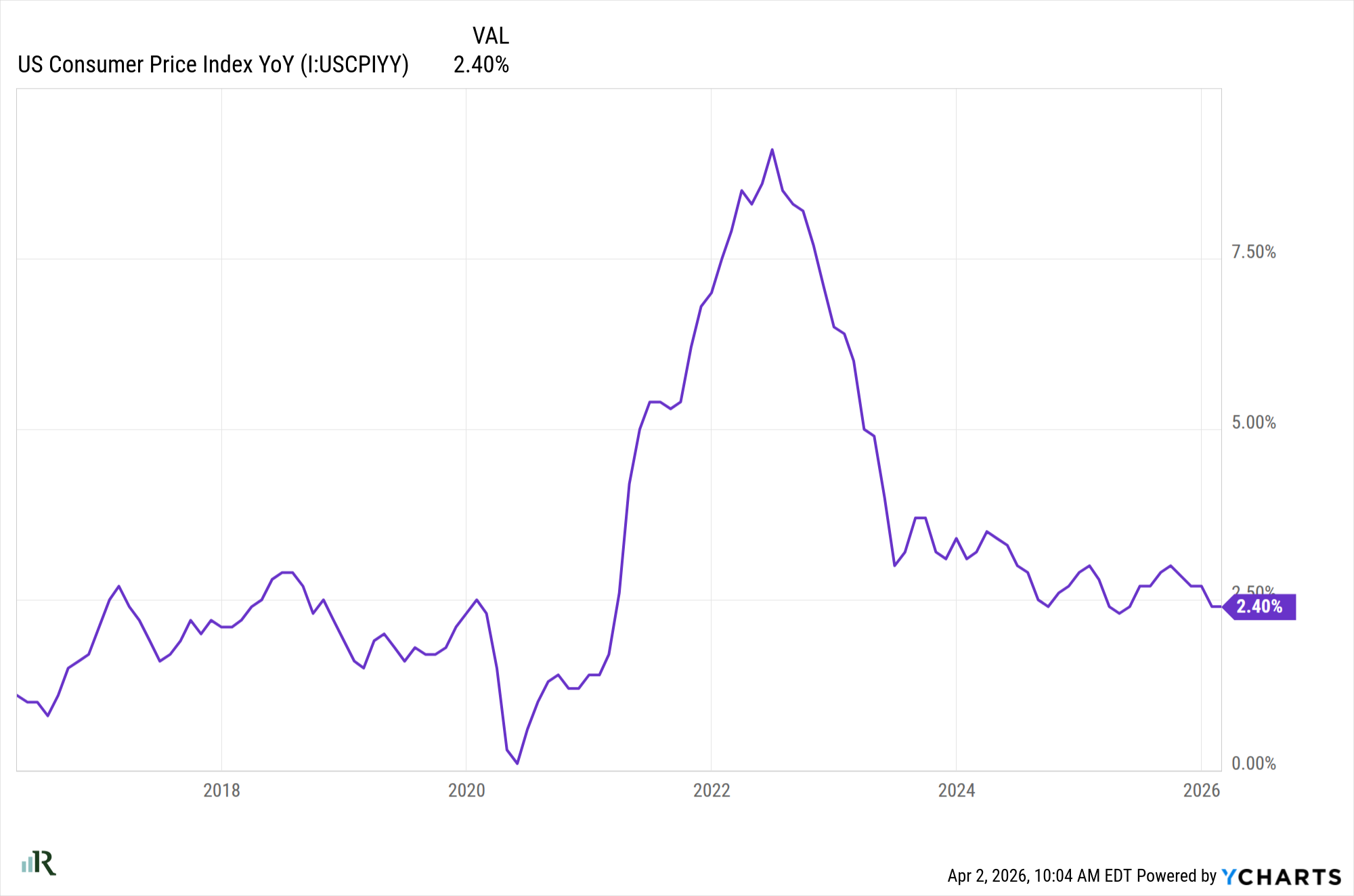

Inflation

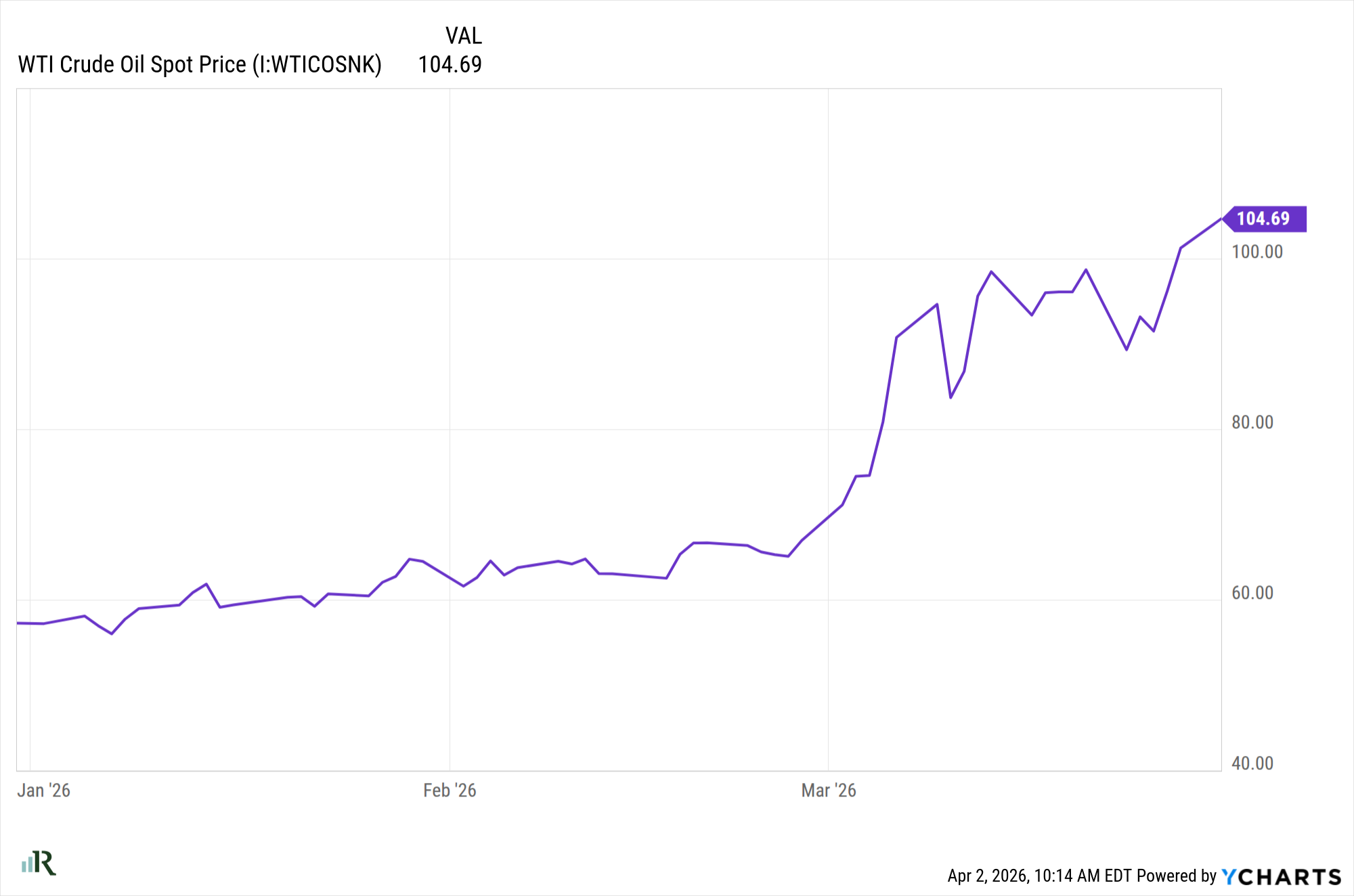

The recent rise in oil prices (from the mid-$60s to over $100 per barrel) is likely to have a meaningful impact on inflation. Since 2022, the Federal Reserve has been working to bring inflation back toward its 2% target, with the most recent February reading showing progress at 2.4%, albeit gradually. However, in the months ahead, inflation as measured by the Consumer Price Index (CPI) could move back toward the 4% range.

The implications extend well beyond higher fuel costs. Elevated energy prices tend to make inflation more persistent, placing additional pressure on consumers to prioritize essential spending over discretionary purchases. This dynamic can weigh on overall economic growth. At the same time, interest rates are likely to remain higher for longer— not only in the U.S., but across global markets— as central banks respond to renewed inflationary pressures.

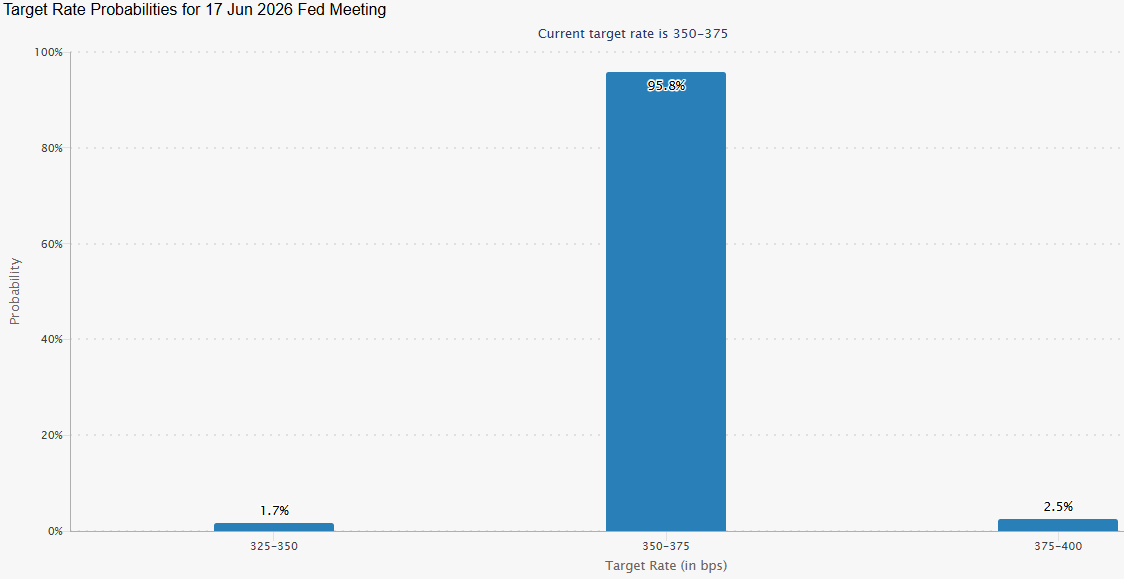

Interest Rates: Cuts Less Likely

One of the most direct effects of higher inflation is its impact on the path of interest rates. At the start of 2026, it was widely expected that the Federal Reserve might lower rates three to four times over the course of the year. Today, expectations have shifted significantly, with current forecasts pointing to zero or possibly just one rate cut. As reflected in the charts below, there is even a modest probability that rates could move higher.

That said, the outlook remains fluid. One potential scenario would involve the Federal Reserve pivoting toward rate cuts if the labor market shows signs of meaningful weakening. As a result, monitoring employment trends will be especially important in the months ahead.

Source: CME FedWatch Tool – CME Group

Stagflation

Stagflation is emerging as a likely scenario over the next couple of quarters. This environment is characterized by rising inflation alongside slowing economic growth, and it is often accompanied by increasing unemployment as companies look to manage costs. While this combination can present challenges, it’s important to remember that, like all economic cycles, it is not permanent— though historically, such periods can persist for some time.

As we enter the second quarter of 2026, there are clearly economic and market challenges to navigate. However, it is not a foregone conclusion that stocks will struggle. Outcomes will largely depend on positioning, as certain sectors have historically performed better in a stagflationary environment— namely utilities, energy, and consumer staples. The range of potential outcomes remains wide, with the trajectory of oil prices likely to play a significant role in shaping the path forward.

Periods like this can make it easy to become overly negative, especially as headlines focus on worst-case scenarios such as recession risks, sharply higher oil prices, or prolonged geopolitical conflict. While these narratives can be unsettling, we believe it is important to stay grounded in data and evidence rather than reacting to emotion or speculation. Maintaining a disciplined, long-term approach remains key during uncertain times.

Information as of 4.7.26

Securities offered by Registered Representatives through Private Client Services, Member FINRA/SIPC. Advisory products and services offered by Investment Advisory Representatives through Rockport Wealth LLC, a Registered Investment Advisor. Private Client Services and Rockport Wealth LLC are unaffiliated entities. The opinions contained herein are that of the authors not necessarily that of Private Client Services LLC and there should not be any guarantees assumed from the information presented.

Investments in securities do not offer a fixed rate of return. Principal yield and/or share price will fluctuate with changes in market conditions, and when sold or rendered, you may receive more or less than originally invested. No system of financial planning strategy can guarantee future results. Investors cannot directly invest in indices. Past performance does not guarantee future results. The performance numbers we mention are indexes. If you’re a client, we manage a custom portfolio for your particular situation and the performance will be different. You cannot invest directly in an index. Investing in an index fund involves fees and will reduce your overall return compared to the index.

Charts produced at yCharts.com

Rockport Wealth Advisors is a DBA of Rockport Wealth, LLC, a fee-based Registered Investment Adviser (RIA) registered with the Securities and Exchange Commission and offering a full range of professional services. The scope of any financial planning and/or consulting services to be provided depends upon the needs of the client and the terms of the engagement. Please see our CRS & ADV disclosure documents for more information about our business.