Rockport Market Update – December 2025

Key Takeaways

-

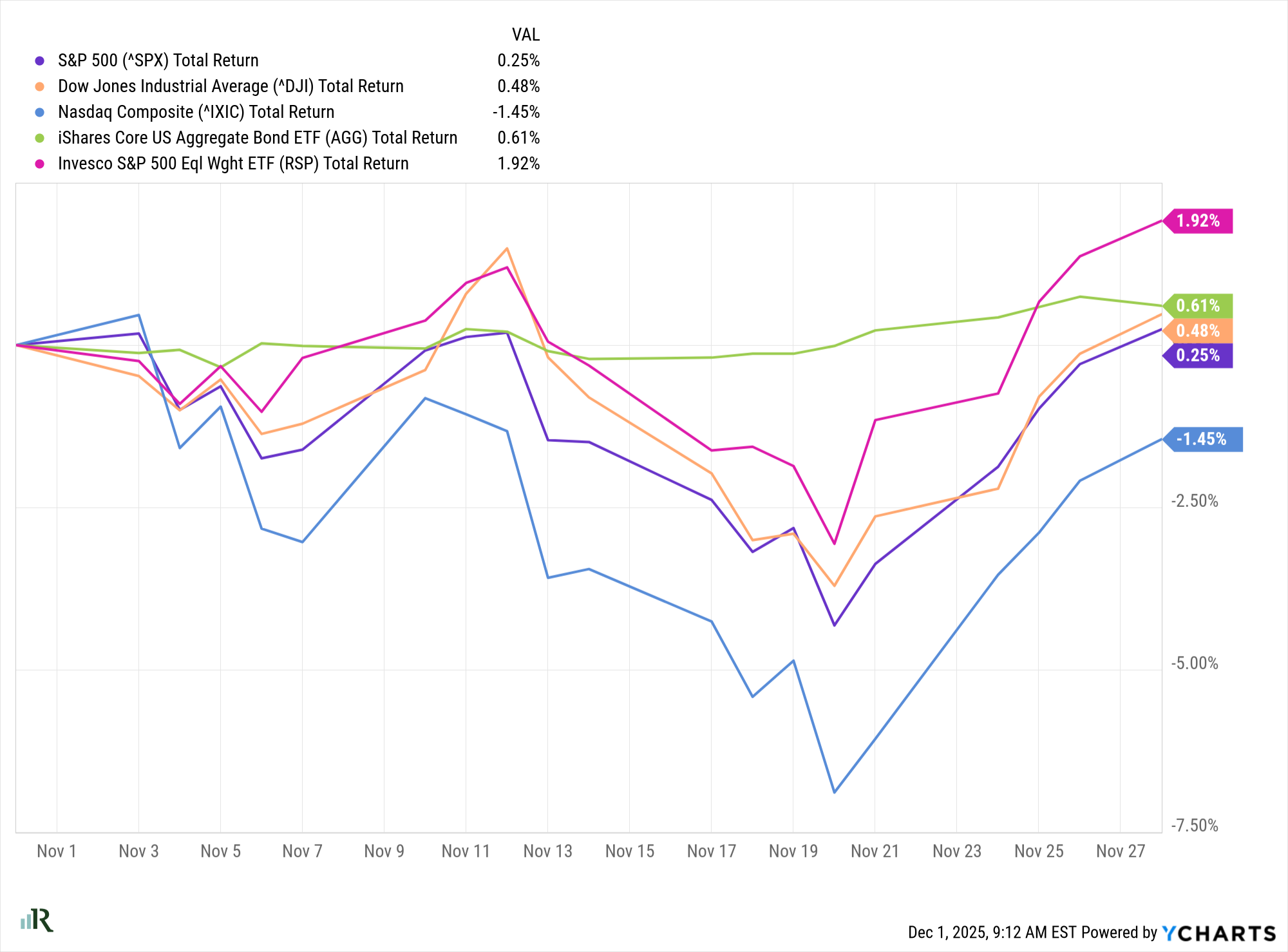

Markets show signs of fatigue early in November, but rebound by month end for slight monthly gain

-

Consumer sentiment slips to multi-year lows

-

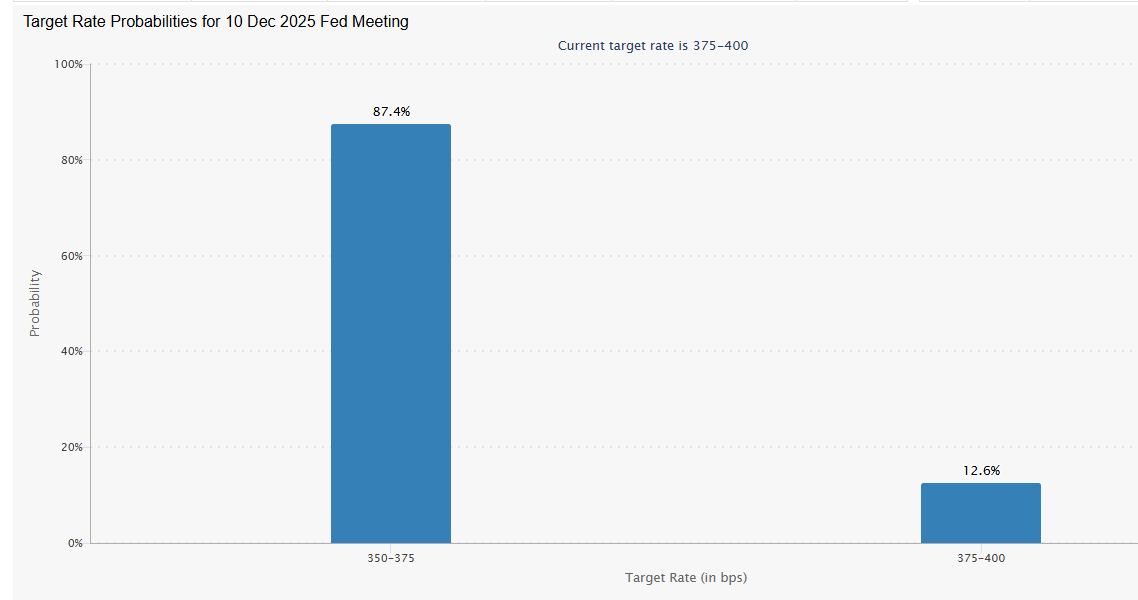

Interest rate cut likely in December (for now)

Stock Market Recap: A Strong Finish to November

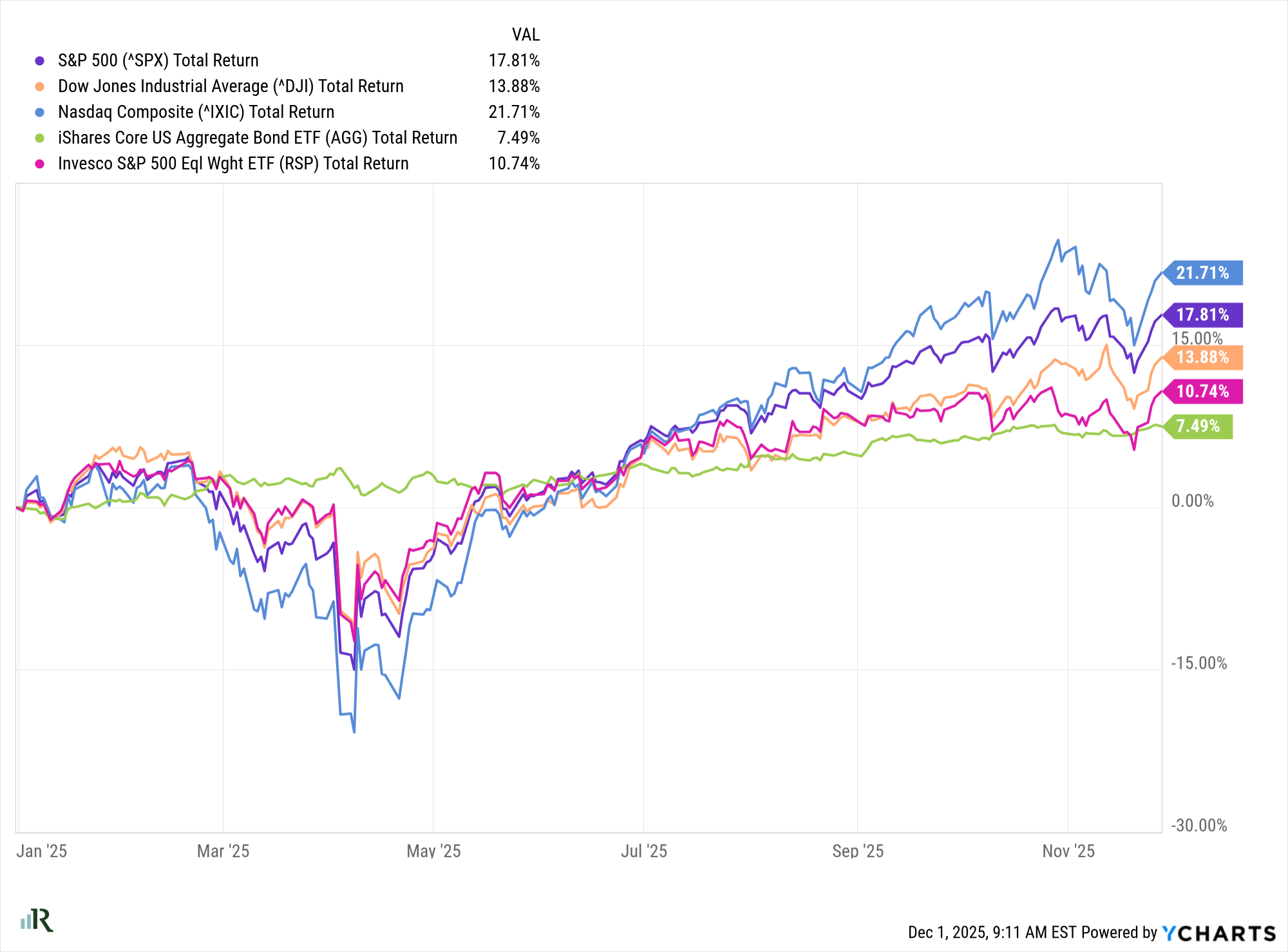

After a shaky start and mid-month selloff that saw major indexes drop more than 5% at one point, the market rebounded by month’s end to close in positive territory. The S&P 500 returned 0.25% for November, lifting its year-to-date gain to 17.81%.

Leading the charge among major U.S. indexes, the NASDAQ has delivered a 21.71% gain year-to-date, while the S&P 500 Equal Weight Index has risen 10.74%.

With such strong performance so far, here’s hoping the market continues its momentum for a positive finish to what has already been a remarkable year.

Consumer Sentiment

According to the University of Michigan Surveys of Consumers, the headline Michigan Consumer Sentiment Index dropped to 51.0 in November— down from 53.6 in October.

The decline reflects increasingly negative views of personal finances, buying conditions, and economic/business expectations.

The November drop suggests that many households are growing more cautious: financial and economic uncertainty— on top of persistent inflation— is beginning to tilt mood downward. Consumption patterns could reflect more restraint, especially on discretionary or big-ticket purchases.

That said: while confidence has eroded, the sentiment indices remain historically volatile. It’s not clear if this represents a long-term shift in consumer behavior or a temporary dip tied to short-term events (shutdown, data blackout, recent price pressures).

Interest Rates

The possibility of Interest rate cuts is back to “likely” for December after a short period in early November where cuts appeared much less likely. The brief period of “less likely” interest rate cuts was due to several factors:

- Hawkish tone from the Fed— internal division and caution

- Minutes from the Fed’s late-October meeting revealed that many policymakers were opposed to further rate cuts. That “hawkish hold” cast doubt on markets’ prior assumption that a December cut was almost certain. (Source: Reuters)

- The central bank also signaled it would end its “quantitative tightening” (QT) program while pausing on new rate cuts — suggesting they felt less urgency to ease further, and wanted to watch how the economy develops before acting.

- Sticky inflation and persistent price pressures

- Inflation remained “sticky”: progress toward the Fed’s 2% long-term inflation goal was incomplete. Price pressures— especially in housing, services, and wages— continued to complicate the decision to cut rates.

- Given that inflation was still elevated, a premature cut risked reigniting inflation— something the Fed seemed wary of.

- Labor-market data and economic uncertainty

- While the labor market was showing some signs of softness, it wasn’t weak enough to make a rate cut a no-brainer. Some economic indicators suggested modest job growth or only limited softening— making it harder for the Fed to justify aggressive easing.

- At the same time, a recent period of delayed economic data— owing to a government shutdown — muddied the picture. That lack of clarity made officials more cautious about cutting until they had reliable, up-to-date information.

Source: CME FedWatch Tool – CME Group

As we move into the final month of the year, market conditions and seasonality remain mostly favorable and the S&P 500 has marked seven straight monthly increases. Continued strength in corporate earnings with inflation stabilizing and bond yields drifting modestly lower are generally supportive of higher stock prices. However, several risk factors and headwinds still exist in the form of narrow market breadth, high valuations and uncertainty about future interest rate cuts which need to be accounted for.

Information as of 12.9.25

Securities offered by Registered Representatives through Private Client Services, Member FINRA/SIPC. Advisory products and services offered by Investment Advisory Representatives through Rockport Wealth LLC, a Registered Investment Advisor. Private Client Services and Rockport Wealth LLC are unaffiliated entities. The opinions contained herein are that of the authors not necessarily that of Private Client Services LLC and there should not be any guarantees assumed from the information presented.

Investments in securities do not offer a fixed rate of return. Principal yield and/or share price will fluctuate with changes in market conditions, and when sold or rendered, you may receive more or less than originally invested. No system of financial planning strategy can guarantee future results. Investors cannot directly invest in indices. Past performance does not guarantee future results. The performance numbers we mention are indexes. If you’re a client, we manage a custom portfolio for your particular situation and the performance will be different. You cannot invest directly in an index. Investing in an index fund involves fees and will reduce your overall return compared to the index.

Charts produced at yCharts.com

Rockport Wealth Advisors is a DBA of Rockport Wealth, LLC, a fee-based Registered Investment Adviser (RIA) registered with the Securities and Exchange Commission and offering a full range of professional services. The scope of any financial planning and/or consulting services to be provided depends upon the needs of the client and the terms of the engagement. Please see our CRS & ADV disclosure documents for more information about our business.